Signal Clustering Predicts Market Volatility

A Cross-Domain Discovery: The Same Pattern That Predicts Pitcher Injuries Predicts Bitcoin Events

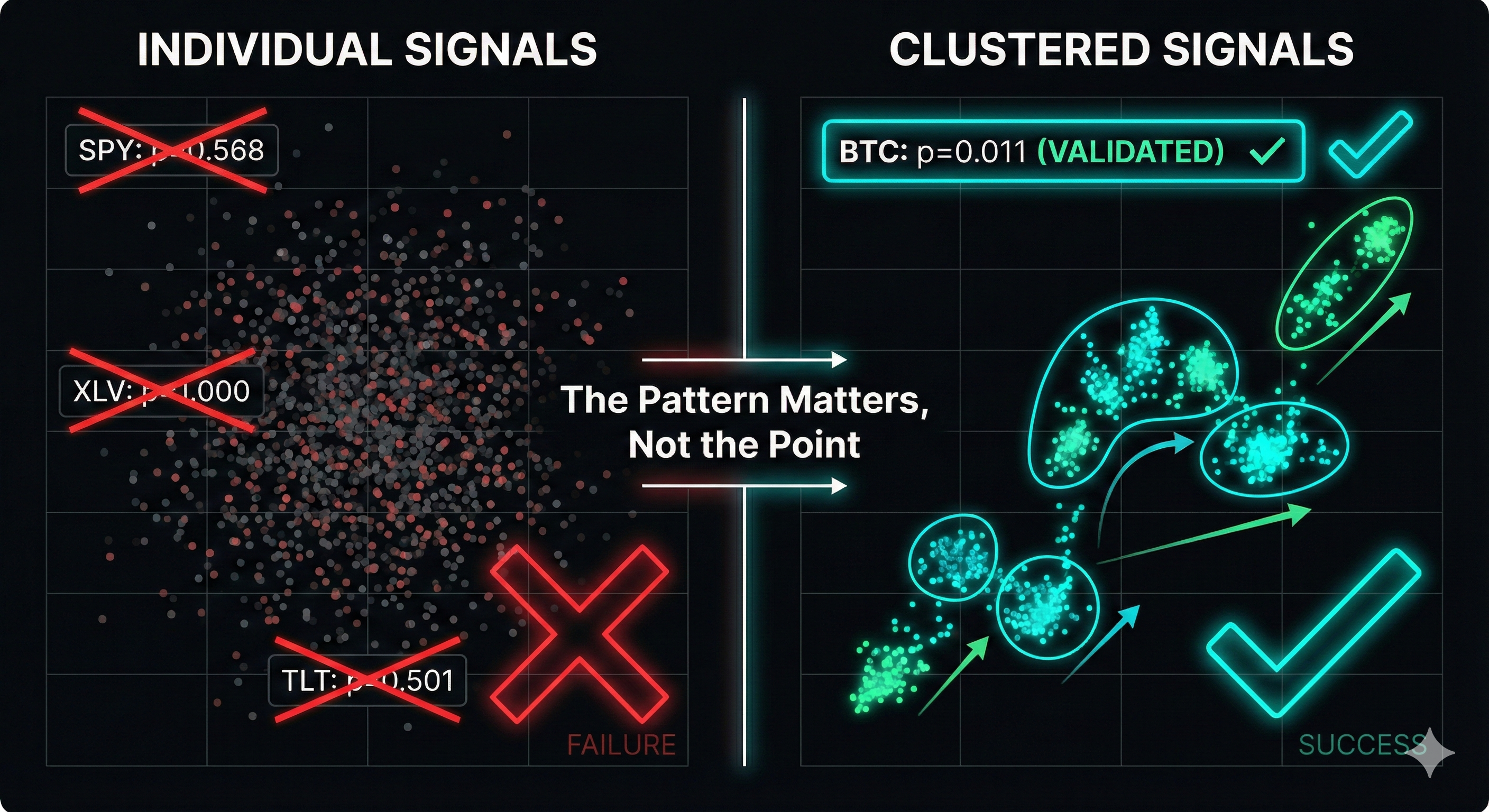

Individual anomaly signals are noise. But when signals cluster together - 2 or more within 14 days - they predict major market events with 98.9% statistical confidence. This is the same pattern we discovered in MLB pitcher injuries, suggesting a universal principle in complex systems approaching critical transitions.

Clustered Signals Predict Major Events

When TRIAXIS detects multiple behavioral anomalies within a short window, it signals that the system is under sustained stress - and a transition is coming.

Bitcoin Signal Clustering: Validated at 98.9% Confidence

Bitcoin 2015-2024: Signal clusters preceded 9 major events including the 2017 peak, COVID crash, and FTX collapse

The Same Pattern Appears in Pitcher Injuries

In a separate study, we found that MLB pitcher injuries follow the same pattern: individual anomaly days are noise, but clustered anomalies predict injury with 84% accuracy. This suggests TRIAXIS detects a universal principle.

| Domain | Individual Signals | Clustered Signals | Lead Time |

|---|---|---|---|

MLB Pitchers Arm injury prediction | Noise | 84% injury prediction | 24 days |

Bitcoin Major event prediction | Noise | 28% event rate (p=0.011) | 36 days |

Complex systems under stress cluster their warnings before failure - whether biological or financial

Why Clustering Works

Normal Variation

Every complex system has occasional anomalies - this is noise, not signal

Sustained Stress

When anomalies cluster together, the system is under real pressure

System Transition

Major change follows within weeks - injury, crash, or rally

Why Bitcoin?

Less efficient than equities, more retail-driven, with dramatic 50%+ events that create clear signal-to-noise

Why Not Equities?

Equity ETFs are too efficient - clustering effects exist but are too weak for statistical significance

Why Pitchers?

Single biological system under repeated stress - similar dynamics to a single asset under market pressure

Individual Signals vs. Clustered Signals

The key insight: it's not about finding anomalies - it's about finding patterns of anomalies.

The pattern matters, not the point

BTC Cluster Monitoring Protocol

How to use signal clustering for Bitcoin risk management

Signal Definitions

When a Cluster is Detected

Recommended Response

| Cluster Size | Action |

|---|---|

| 2 signals in 14 days | Reduce exposure 25%, tighten stops |

| 3+ signals in 14 days | Reduce exposure 50%, prepare for volatility |

| 5+ signals in 14 days | Consider full exit or hedge |

Important: Risk Management, Not Trading Signals

Clusters predict volatility, not direction. 72% of clusters will not precede events (false alarms). Use this for risk management - reducing exposure before potential turbulence - not for placing directional bets.

Methodology

Data

- 18 years of equity ETF data (SPY, XLV, TLT, DIA, XLI)

- 10 years of cryptocurrency data (BTC-USD, ETH-USD)

- 77-dimensional behavioral feature vectors from OHLCV

- 9 catalogued Bitcoin events, 13 market events

Validation

- Monte Carlo simulation with 1,000 random trials

- p-value = (trials >= real performance) / 1,000

- Significance threshold: p < 0.05

- BTC clustering: p=0.011 (VALIDATED)

Signal Detection Process

- 1.Submit 60-day rolling windows to TRIAXIS engine

- 2.Calculate rolling z-scores of anomaly rates (252-day baseline)

- 3.Flag dates where z-score > 2.5 as "signals"

- 4.Identify "clusters" as 2+ signals within 14 days

- 5.Validate against catalogued events via Monte Carlo

Key Takeaways

Signal Clustering is Validated

Bitcoin clusters predict major events 2.8x better than random with 98.9% statistical confidence

Cross-Domain Pattern

The same clustering pattern predicts MLB pitcher injuries (84%) - suggesting a universal principle in complex systems

Risk Management Application

Clusters predict volatility, not direction - use for reducing exposure before turbulence, not for trading signals

Scope Limitation

Validated for Bitcoin only - equity ETF clustering effects are too weak for statistical significance

Research Disclaimer: This paper presents historical analysis. It does not constitute investment advice or trading recommendations. Past performance does not indicate future results. The 72% false alarm rate means most clusters will not precede events.

Want the Full Research?

Request the complete whitepaper with detailed methodology, event catalogs, and statistical validation.